Wynnewood Gardens: 106-Unit Case Study

Looking to get in the market? It's for sale!

This is a story I’ve been wanting to write for a long time. Many of you know that I started in real estate with a 4-plex in Silicon Valley. It was a house hack gone wrong, or perhaps gone wildly right.

When I sold the property, I had no idea what I was going to do next. I found myself flying around the country in a frantic search for a property I could buy with the extra $500K that would otherwise go to the government in taxes. Just in the nick of time, I was lucky enough to find a 106-unit property in Dallas, Wynnewood Gardens.

Today I want to share with you the story of this property, how I thought about the purchase, what made it sound at the time, and how it has performed.

Additionally, I’m pleased to let you know that Wynnewood is currently for sale! If you are looking to get into the market, perhaps it could be a good fit for you.

Full disclosure, I posted parts of this story on Twitter last week. Likes and retweets are most appreciated.

Property Info

Units: 106

19 buildings on 6.02 acres

Year of Construction: 1947

To those of you from New York, Los Angeles, and many other established parts of the country, a 70-year-old building is young. But in a young city like Dallas, it’s very unusual.

Most of the buildings I had looked at in my search were late 1960s - early 1980s. The main reason older buildings don’t exist is that the low-density communities on choice plots of land have been razed and redeveloped into Class A luxury apartments.

Older buildings tend to generate less interest from buyers for good reason; with many of the core building systems toward the end of useful life, the next ownership group could be on the hook for expense upgrades.

But Wynnewood Gardens was different. It was old enough that the major building systems had already been replaced. It has:

Pitched, composition roofs

Copper water plumbing and PVC sewer

Copper electrical wiring

Individual HVACs

Individual hot water heaters

Washer/dryer connections in every unit

Which as a package are typical of 1980s and newer construction. As a result, Wynnewood, with its solid brick exterior, is probably more solid than the 1960s and 1970s product I was looking at.

Ideally, the winning bidder in a competitive auction finds a key piece of information that everyone else has overlooked. For me, this was the idea that the effective age of the building could be much lower than its physical age, and that it could also be acquired for a much lower basis than its younger counterparts.

Location

Always consider location at different levels of zoom.

I won’t even comment on the growth of Texas and the Dallas metroplex. It has been tremendous for years.

The growth trajectory of the neighborhood surrounding Wynnewood was equally exciting. It sits about two miles from the red hot Bishop Arts District, and along the I-35S corridor which is very much the path of progress, filled with construction and redevelopment.

In addition the general neighborhood, the street level location is phenomenal. Wynnewood is on the corner of a major intersection, Zang and Illinois are two of the busiest streets in the area.

Plus, it’s directly across the street from Wynnewood Village, a 65-acre shopping center owned by the REIT Brixmor.

Most excitingly, Brixmor (with the City of Dallas’ heavy blessing and financial support) is investing $30M to redevelop the mall. You’ve got to be excited when your neighbor spends $30M of their own money to improve the area!

Finally, there is no competition in the area. There are only two other market-rate properties within ~1 mile, and one of them is currently undergoing a $35k/door renovation. So both public REITs and private ownership groups believe that now is the time to reinvest in the area.

The Deal Structure

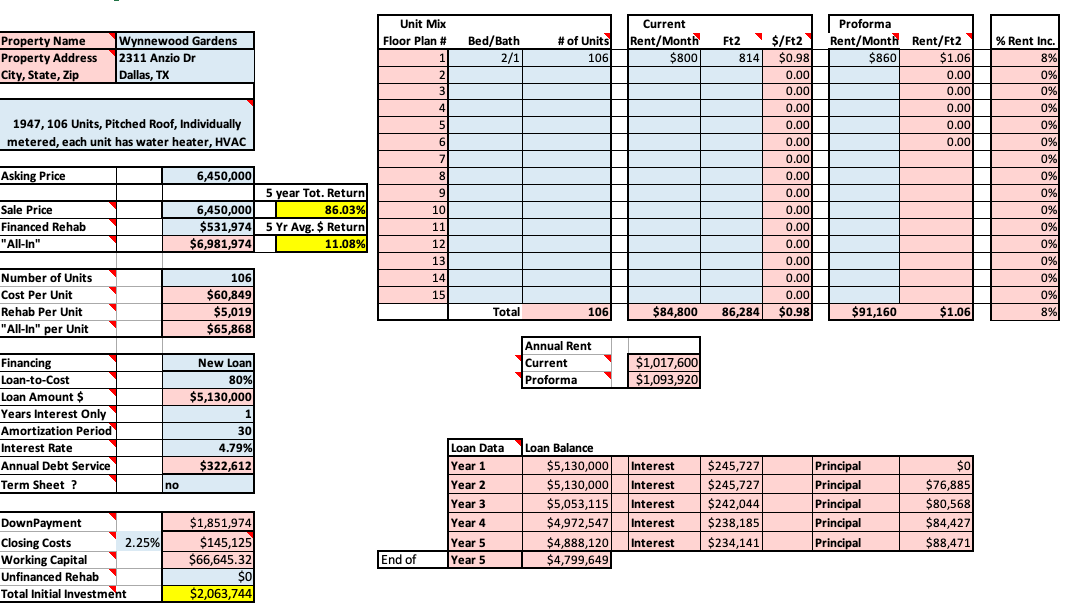

Purchase Price: $6.45M ($61k/unit)

Rehab Budget: $530K ($5k/unit)

Loan: $5.13M (80 LTV) @ 4.79% fixed for 12 years

For those of you who are familiar with current pricing (hint: it’s a lot higher now!) you should know that when I bought the deal, it felt like overpaying.

Price growth had been egregious during my search. The seller paid $3.3M for the property in June 2016. They spent under $100K on rehab — literally did almost nothing — and then sold it to us 18 months later for double the price. Talk about perfect timing! I estimate that they at least quadrupled their equity.

Would that comfort you, or scare you?

Coming off of a difficult 1031 exchange, I thought that I never wanted to bother with one again and that I would hold Wynnewood forever. Accordingly, my mortgage broker advised me to lock in the historically low rates for as long as possible.

Things have changed, obviously. Now that I’m looking to sell, I will have a $1.3M prepayment penalty since the 10Y treasury yield has fallen. For an extra ~15 bps interest rate, this could have been avoided. I’m beyond upset about this; hopefully I will only have to learn this lesson once.

Underwriting

I’m going to walk you through the exact underwriting that I used.

The left column shows the deal parameters that I mentioned above: purchase price, rehab dollars that were rolled into the loan, the interest rate and amortization. We spent an additional ~$150k on closing costs, which is on the low end.

The top-right chart shows that there is only one floor plan, a 2BR/1BA @ 814sf, that was renting for $800. The entire underwriting was premised on being able to achieve the pro forma rent, $860, after completing our renovations.

The box in yellow shows the predicted ~11% average yearly cashflow during the hold period and that the total return including appreciation would be ~86% after 5 years.

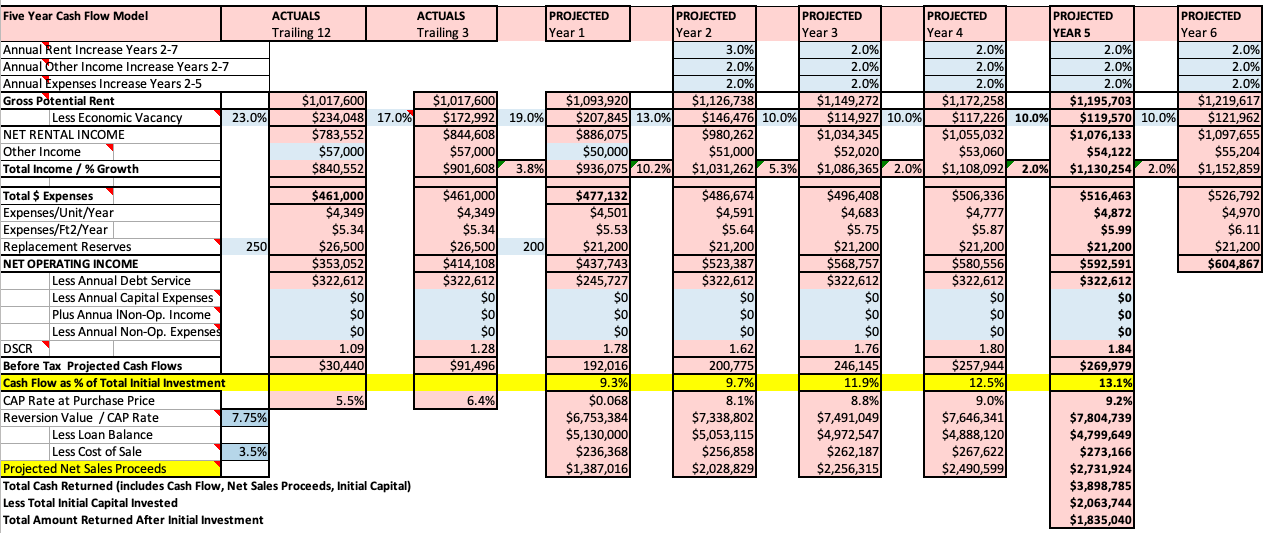

This page shows a five year cashflow model. The assumptions are highlighted in blue.

Starting from the top: I assumed a 3% rent increase the first year and 2% in subsequent years. I assumed expenses would grow at 2% each year.

Economic vacancy is a concept that combines physical vacancy (rent you don’t collect because nobody is living there) with collection loss from concessions, nonpayment, and rents that are below market.

Even though my hope was to have a building that was always at 100% occupancy at the highest rents in the submarket, I projected that there would always be at least 10% economic vacancy, as a conservative measure.

Finally, I assumed the cap rate that the next buyer would value the property at would be 7.75%. This turned out to be extremely conservative, as the property will probably be sold at under a 5% cap! This means the purchase price will be ~55% higher than I projected.

Let me also take the opportunity to say a few philosophical words on underwriting in general.

Underwriting is always wrong. The only questions are: how wrong, and in which direction?

It’s a Goldilocks problem. You don’t want to be too conservative, because then you’ll never win a deal in today’s market. But you also don’t want to be too aggressive, because you’ll lose your money.

I find that the best approach is to combine justifiable optimism in some areas with reasonable pessimism in others. Since the cap rate is the number that most affects returns in the entire underwriting, I find that being conservative with the exit cap rate can forgive a lot of mistakes.

This chart shows what the seller’s expenses were, and what I projected them to be. Of note

I expected to save money on utilities by performing water conservation

I thought we could significantly cut payroll costs

I expected property taxes to increase significantly post sale

The actual numbers were based on the property performance history and consultation with my property management company, tax consultant, insurance agent, and water conservation consultant.

Rehab

At the time, $5k/door seemed like a large rehab budget, and sufficient for our aspirational plans. But it turned out not to be enough due to the amount of deferred maintenance we had to cure.

Although they weren’t leaking, the roofs were in rough shape. We filed a claim against the seller’s insurance because there were recent severe hail storms, but were turned down.

At the suggestion of our co-purchaser, who was 30 years more experienced, replacing all of the roofs was the first thing that we did. Fortunately, we have not had any leaks, but this ate up ~33% of our rehab budget. Once you tear off the roofs, you may as well replace the gutters and fix the fascia and eaves to do it properly.

Then we had to resurface the parking lot and replace many sections of sidewalk. Here is a map of all of the areas of sidewalk that needed patching or replacing.

We also spent a great deal of money on landscaping to fix years of erosion and install a drainage system so that it wouldn’t happen again.

All of this cut significantly into our rehab budget. As a result, some of the aspirational exterior work had to be cut. One item of note that we did complete was to redo all 106 porches and decks.

This was a fantastic project because it removed a major eye sore and allowed us to raise the rents ~$25/month for the improved amenity.

The rest of the rehab budget was spent on interior renovations. Because we didn’t have outside investors, I reinvested ~$300K from operational cashflow to further improve the property.

Lessons for future projects:

Maximize rehab spend on items that allow you to raise rent

Tackle exterior improvements first. That's how you'll attract better tenants.

Pad your rehab budget. You will go over budget and find additional deferred maintenance.

Performance

We increased average monthly income from $74k/mo at purchase to over $100k/mo now. (I’ve inserted the maximum number of images, so if you want to see the charts I’ll refer you to the tweet)

If you’ll recall, my pro forma dependent on achieving $860/month base rent and growing at 2% per year.

Well, our base rent is now $975/month, which is $60 above projections.

Not only that, we have recently begun investing in premium-level unit upgrades with

new cabinets

stainless steel appliances

subway-style backsplashes

We are renting these units for $1150/month! Here is what they look like.

Sale & Opportunity for the Next Buyer

The next owner has the opportunity to create $5M+ value with a relatively light lift. Here's how I would do it.

First, continue the proven premium unit upgrade program as shown above.

A $175 premium (rent goes from $975 to $1150) is another ~$200k/yr in new income. That’s ~$4M in value created.

Second, Wynnewood owns 30-40 washer/dryer sets, but only ~10 tenants are paying for them. I'd buy sets for every unit and rent them for $50/month.

Using cap rate math, an extra $60k/yr is $1M in value created.

Third, address parking. The property has both open and covered spots, but the covered spots are more desirable, and residents will pay for them.

40 units paying $35/mo is an extra $16k/yr, or $300k in value created.

Finally, a technology package. Neighboring properties are getting master contracts for cable and wifi and then re-selling them to residents. There's ~$25/unit/month profit in both cable and internet packages.

Call it an extra $30k/yr, or $600k in value for each.

You're probably wondering, why are you selling if you believe all of this?

It goes back to my loan. As the value of the building has increased, my return on equity is very low. But I can't refinance and a supplemental is not an attractive option to pull out equity.

I’ve also exhausted my rehab budget, so I lack the capital to take the property to the next level. A new owner with fresh capitalization is better able to give the property what it needs.

Conclusion

I hope you found this interesting and informative; I’ve tried to be a rather open book.

Feel free to reach out to me if you have questions, and feel free to share this with anyone who may be interested in bidding on the property. The call for offers date is this Thursday, October 21.

Hello there,

Huge Respect for your work!

New here. No huge reader base Yet.

But the work has waited long to be spoken.

Its truths have roots older than this platform.

My Sub-stack Purpose

To seed, build, and nurture timeless, intangible human capitals — such as resilience, trust, truth, evolution, fulfilment, quality, peace, patience, discipline, relationships and conviction — in order to elevate human judgment, deepen relationships, and restore sacred trusteeship and stewardship of long-term firm value across generations.

A refreshing take on our business world and capitalism.

A reflection on why today’s capital architectures—PE, VC, Hedge funds, SPAC, Alt funds, Rollups—mostly fail to build and nuture what time can trust.

“Built to Be Left.”

A quiet anatomy of extraction, abandonment, and the collapse of stewardship.

"Principal-Agent Risk is not a flaw in the system.

It is the system’s operating principle”

Experience first. Return if it speaks to you.

- The Silent Treasury

https://tinyurl.com/48m97w5e